BBS is technique number 15 in our Business Analysis Techniques book of 99 essential BA tools. It was developed by Robert S. Kaplan and David P. Norton as a means of defining a framework of performance measures that would support the achievement of the vision for an organisation, and the execution of its business strategy (Kaplan and Norton 1996).

BBS is technique number 15 in our Business Analysis Techniques book of 99 essential BA tools. It was developed by Robert S. Kaplan and David P. Norton as a means of defining a framework of performance measures that would support the achievement of the vision for an organisation, and the execution of its business strategy (Kaplan and Norton 1996).

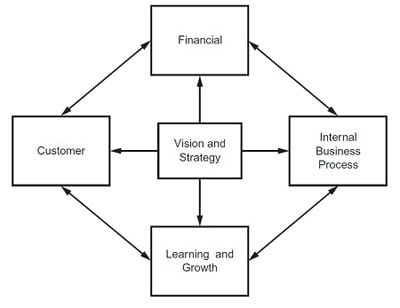

Historically many organisations, and external stakeholders such as shareholders, have focused on their financial performance. However, financial measures have typically related to past performance, and the decline of financially stable organisations can be attributed to a lack of attention to areas of performance that will generate success in the future. The BBS identifies four aspects of performance that should be considered:

Financial: This aspect considers the financial performance of the organisation, looking for example at the profit generated by sales, the returns generated by the assets invested in the organisation, and its liquidity.

Customer: Looking at the organisation from the customer perspective shows how customers view it. For example, the level of customer satisfaction and the reputation the organisation has in the marketplace are considered.

Internal business process: This perspective shows the internal processes and: procedures that are used to operate the organisation. For example, are the processes focused on reducing costs, to the detriment of customer service? Is the technology used well to support the organisation in delivering its products and services?

Learning and growth (also known as innovation): The learning and growth perspective is concerned with the future development of the organisation. Examples of performance areas are the development of new products and services, the level of creative activity in the organisation, and the extent to which this is encouraged.

The approach to identifying critical success factors (CSFs) and key performance indicators (KPIs) is usually used in conjunction with the BBS. The Mission and Objectives of the organisation are used as the context in which to define the BBS areas. For example, if the Mission is to deliver good value, high quality services to customers, then the four BBS areas could measure performance as follows:

- financial - level of supplier costs;

- customer - prices charged in comparison with competitor prices;

- internal - quality checking processes;

- innovation - introduction of new products.

The BBS helps ensure that organisations will not focus solely on financial results, but will consider both their current performance and the factors that will enable continued success.

The BBS is used to ensure that a complete view of the organisation’s performance is measured and monitored. It is vital that all four areas are considered, not just one or two; omitting any of the areas is to risk undermining the performance of the organisation, and to increase the chance of business problems arising in the future.

If you found this technique useful and would like to read more, visit www.bcs.org/books/batechniques