What if, one day, it cost twice as much to run oil wells, or to mine iron and gold? Perhaps not a perfect analogy, but should industrial demand for these commodities remain the same, increased cost of production ought to lead to an increase in prices.

If the date of these cost increases were known in advance, speculation might drive prices up well in advance. And that is the key thing: demand in terms of practical use would lead to an increase in price.

Something of this nature, called ‘halving’, took place on the 11th of May 2020 in the world of pioneering crypto-token Bitcoin. As you read on, we’ll explore what the halving was and why it happened.

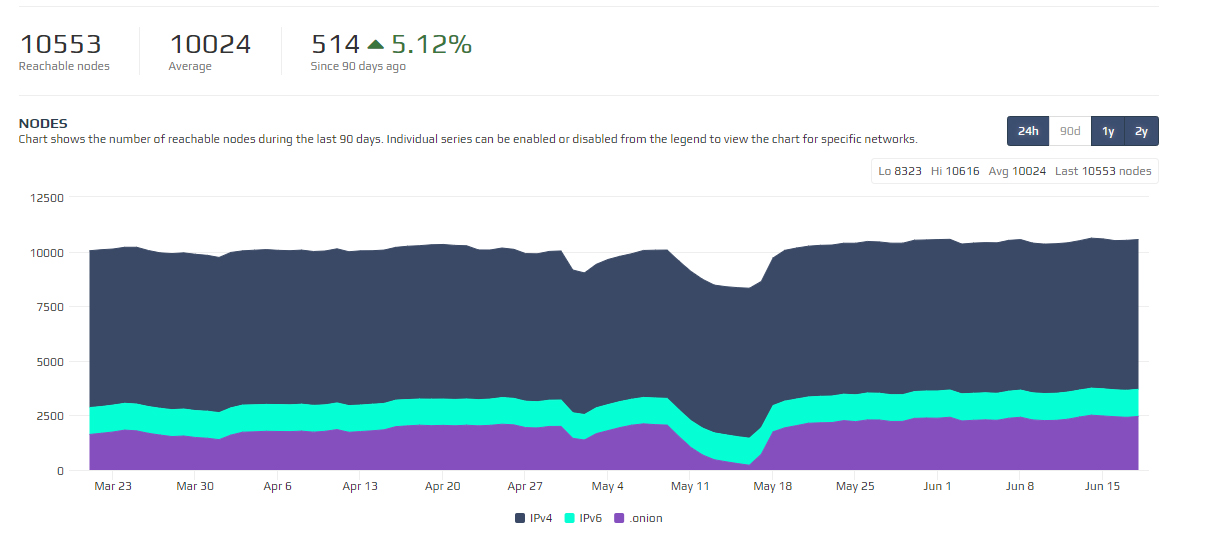

Fig 1: bitnodes.io shows a dip in number of Bitcoin nodes around the halving event, followed by recovery to 90-day normal (graph used with permission). Readers who examine the price graph of Bitcoin in the weeks leading up to the halving event, should notice a similar dip followed by a recovery, which may or may not have any relation to the halving. (click to view larger image)

Money, assets and speculation

For this analysis, let us first examine the role of both traditional money and gold as assets. Typically, economists and financial advisers do not consider money as an asset. Money is either saved or invested in asset classes like interest-earning deposits or bonds, equities, commodities and other assets.

Investments are made with an expectation of gain, either from capital appreciation via future price rises, or the possibility of recurring revenue, like dividends from shares in a company; at least to save value from being eroded via inflation. The magnitude of these expected gains allows investors to put a value (and therefore, price) typically denominated in traditional currency.

Gold, for instance, is a rare and precious metal with many uses. Oil has more widespread use in the global economy, even if one would hope for a shift to renewable green energy. And, since Bitcoin is often seen as analogous to gold due to the difficulty of its production and finite quantity, it is supposed to retain value - unlike traditional currencies.

There is one key difference though: Bitcoin’s only known practical uses are a) to pay transaction fees to the blockchain network, that in turn offers the immutable public ledger as a service, and b) as a possible medium of exchange of value, which is a role fulfilled by traditional money.

The making of money

A unit of traditional money comes into being as a result of debt1. This means, when a government needs to raise funds, one of the means to do so is to issue debt bonds. Typically, the country’s (or monetary union’s) central bank quite literally creates an equivalent amount of money that it expects to be repaid with interest.

Until the early twentieth century, a certain amount of gold had to be deposited with the central bank, but this need was removed by most countries decades ago, to fuel post-second world war growth. The money thus borrowed or created, is used to fund various government expenses, indirectly supports profit-making enterprise that in turn leads to expansion of the economy or value creation, finally allowing the debt to be paid back with interest. This is an oversimplification, of course. Debt is not the only method for governments to raise funds; certain government debts such as gilts are also available to the public, not just to banks.

Governments and monetary systems also need to strike a good balance. If they borrow or create too much money, that could lead to uncontrolled inflation or loss of value of the currency.

The difference with cryptotokens

Unlike traditional currency, units of cryptotokens2 like Bitcoin and Ethereum come into being when a node (a computer participating in a blockchain network) successfully confirms a transaction and is paid a certain amount of cryptocoin - known as block reward - for the effort. To be precise, multiple nodes need to independently confirm a block of transactions. This is the point when the new amount is said to be created or mined and the first transfer is made to the wallet of the node(s) that did the work as block reward.

This reward is coded into the network software that runs the blockchain network and has a predefined upper limit. This is why Bitcoin is advertised as being finite in quantity, like gold, but unlike fiat currencies.

Confirming transactions, by calculating hashes of blocks in combination with previous blocks so they are linked, is the main job of participating nodes. This requires work to be performed via computing power. Other costs involved are the capital overlay in purchasing and setting up mining computers and the electricity to run them.

Actual users who rely on these networks to transfer value and record transactions in the ledger also pay a fee for each transaction.

These transaction fees and block rewards have no bearing on the prices of crypto-tokens that we see in the headlines and the purpose of this article is not to comment on whether it is fair. But, for the network to remain viable, these transaction fees would need to, at least, cover the transaction confirmation costs incurred by the mining computers (say, their electricity bill paid in GBP).

Halving

The background covered in the previous section explained the creation of crypto-tokens at a high level. Another feature built into the Bitcoin blockchain is that the new tokens created as block reward are halved after a fixed number of blocks are confirmed.

Even though all blockchain networks do not follow this halving system, their price trajectory still often seems to track Bitcoin’s. For instance, Ether’s price graph around the Bitcoin halving event is roughly the same shape as Bitcoin’s graph for the period.

This indicates that halving was not an event of much consequence and that the price of Bitcoin is driven purely by speculative trading.

Bigger concerns about Bitcoin

Bitcoin’s use as a method of payment has not received widespread acceptance. No major merchants that claim3 to accept Bitcoin actually publish a public Bitcoin wallet address that can be independently verified.

Organisations that do accept Bitcoin - like Wikipedia - do so via in intermediaries. This suggests that they do not actually retain it but immediately convert it into normal currency. Wikipedia publicly lists its bank and other account details to receive donations, yet it doesn’t list a Bitcoin address.

Request to share their public Bitcoin wallet address was answered, but instead of their Bitcoin address, the author was directed to their donations page on payments intermediary BitPay4 (The author found it convenient to make a GBP donation using a debit card). By contrast, the Bitcoin project’s website does list their Bitcoin address and transactions on this can be viewed publicly5.

The primary intended use of Bitcoin is to serve as a direct, peer-to-peer exchange of value without the need for trusted intermediaries. What seems to be more common instead, is speculative trading in Bitcoin via intermediaries described as ‘cryptocurrency’ exchanges.

This model introduced some other problems. An example is wash trading6 - a process whereby an exchange or large trader buys and then sells assets with the hope of feeding misleading information to the market. This simultaneous buy and sell can create the illusion of inflated demand for a security7.

The quantum conundrum

Blockchain systems, in general, might also face another much bigger risk: quantum computing. Quantum computing could have the potential to critically disrupt the process of Bitcoin mining by making the process incredibly fast.

Quantum computing also threatens to break many of today’s encryption systems, which directly threatens the immutability of current blockchain-based ledgers. This is a problem not only for Bitcoin but also other, more widely used systems, based on today’s cryptography. For now, Bitcoin halving, though well-intended, doesn’t appear to be something of major consequence…