Dr Alan Ma MBCS, qualified in IT, engineering and law, shares his insights into the status of the use of blockchain-enabled smart contracts in the industry. Dr Ma is a law lecturer at Birmingham City University.

Blockchain is a distributed ledger made up of immutable blocks of data chained together to create an encrypted history of transactions.

It carries the functionalities of being automatically self-executed, immutable, providing permanent records with real-time information, reducing cumbersome documentation using high processing power and avoiding human errors. These features are attractive for commercial use that involves a large amount of repetitive and similar transactions. The number of industries deploying blockchain-based solutions is growing.

The concept of smart contracts was started by computer scientist, Nick Szabo, in the 1990s. He defined a smart contract as ‘a set of promises specified in digital form, including protocols which the parties perform on those promises.’

Szabo illustrated his definition by reference to a vending machine: a consumer inserts coins into the machine (satisfying the condition of the contract); the vending machine automatically dispenses the chocolate bar (meeting the terms of the contract).

The transaction is facilitated by the software, which enables the transfer of output (the chocolate bar) on the occurrence of input (the correct payment). A smart contract is, therefore, a computer program that has certain inputs and which executes a set of instructions, to come to one of many pre-determined outcomes. The computer code defines obligations between parties and it runs on a blockchain.

Smart contract v traditional natural language contract

Contracts define the obligations and considerations between the parties. The legal principles of contract law are well established and their application is pervasive in our daily life. They form the bedrock of doing business. Contracts written in natural language can be traced back to the Middle Ages – and we have never considered alternative forms until the birth of smart contracts.

With such attractiveness emerging from blockchain technology, can smart contracts replace natural language contracts? A short answer is no, not at present. Smart contracts handle only the pre-determined outcomes programmed in the software. Whereas natural language contracts allow room for courts to interpret the meaning and exercise judgment to maintain justice and fairness. So where are we now?

Click to view larger image.

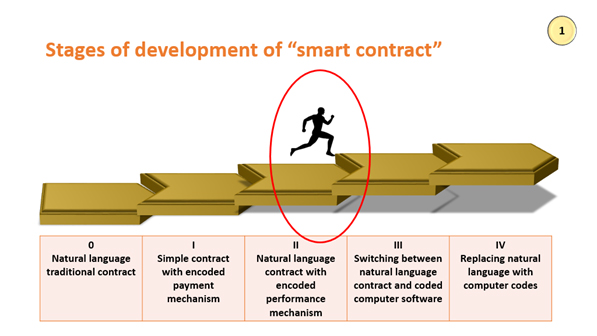

Figure 1 sets out the various stages of the development of smart contracts with the eventuality of replacing natural language with computer codes:

- Stage 0 is the traditional natural language contract.

- The transformation starts in Stage I by writing the straightforward rules-based functions in digital forms responding to specific inputs, like payment is processed when the goods are delivered and verified.

- Stage II extends the rules-based functions to more complex cases, like the automatic deduction of liquidated damages for late delivery of work when the level of damages is pre-estimated and agreed upon before the work starts.

- Stage III is more advanced with interactions between the natural language contracts and coded computer software.

- Stage IV is a replacement of a natural language contract with computer codes.

We are at Stage II, advancing.

The rise of smart contracts

However, even with the limitations, smart contracts are efficient in many ways and generate positive impacts on the contracting lifecycle.

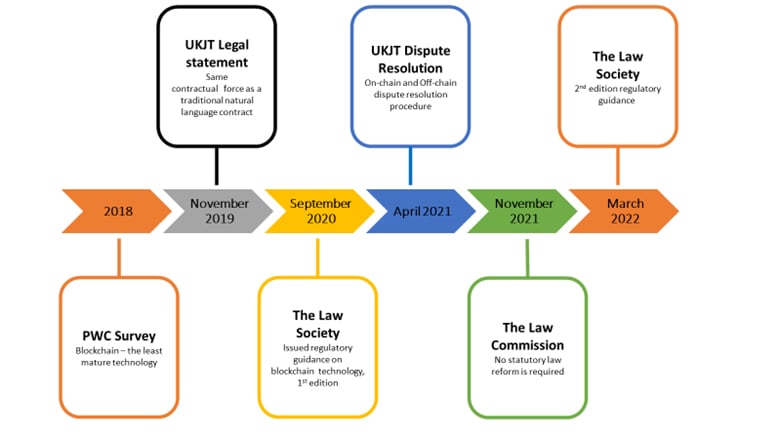

Optimum benefits can only be gained if smart contracts are enforceable, accepted by legal practitioners, regulated by the authorities and recognised by legislators. Figure 2 shows the timeline of the advancement of smart contracts from being the least accepted emerging technology, to becoming an integral part of legal practices and a mainstream area of law.

Click to view larger image.

Four years ago, the legal profession did not embrace blockchain technology with much enthusiasm. A survey done by PWC on the top 100 law firms revealed that blockchain technology was not interested/aware and it was classified as being under research by law firms[1]. The technology was the least mature in the application among other digital technologies at the time, like AI, robotic automation, and predictive analytics.

Current legislation

In 2019, the UK Jurisdiction Taskforce (UKJT) published a legal statement on smart contracts[2]. UKJT is an advisory body with the backing of the UK Government and composes of industry experts from practices, regulatory bodies, and the judiciary.

The legal statement asserts that a smart contract satisfies the legal requirements of creating an agreement between parties and can have contractual force, just like a more traditional or natural language contract.

The rights and obligations written in code are binding and enforceable under English contracts law. The report concludes the common law is capable to respond consistently and flexibly to new commercial mechanisms. Judges can apply and adapt by analogising existing principles to new situations as they arise.

For you

Be part of something bigger, join BCS, The Chartered Institute for IT.

In 2020, the Law Society of England and Wales published regulatory guidance on blockchain technology[3]. This is a formal recognition of the accepted use of smart contracts.

A significant implication of this publication is that every practising lawyer must be conversant with the application and operation of smart contracts. keeping the regulations in sync with other advancements. The second edition of the report was published in March 2022.

In 2021, UKJT extended the legal statement to cover situations when things go wrong[4]. The Taskforce appreciates that not all disputes can be resolved on-chain using the self-executed process.

Arbitration, not court proceedings, is specified to deal with disputes off-chain. Arbitration is a private dispute resolution method and its use can trace back to the 7th century. Unlike court proceedings, it is flexible and the procedure can be modified when appropriate. It avoids any delays caused by setting up a separate court system to deal with digital disputes.

The latest significant publication is the report by the Law Commission of England and Wales[5]. The Law Commission is the statutory independent body to keep the law of England and Wales under review and to recommend reform where it is needed.

The 2021 report concludes that the current legal framework based on English common law is adequate to support the use of smart contracts and that no statutory law reform is needed. The conclusion is significant as legislation takes time to draft, debate, enact and enforce. This conclusion clears the last barrier to applying smart contracts for general application.

What does that mean for the IT profession?

The legal profession is catching up with the advancement of technology behind smart contracts. Not long ago, smart contracts would have been considered as the law of the future and the future of the law – this thinking is now out of date.

The series of reports published by the legislators, the lawyers and the judiciary, means that smart contracts are ready to be put into everyday use. This gives a sense of certainty to users and a major boost of confidence to the IT profession for developing the novel technology.

This brings the IT and legal professions closer as they work on areas to further enhance the available blockchain technology. We are expecting the use of smart contracts to be taken up at a pace that has never been seen before, together with a huge rise in investment in this area and the demand of talents to follow.

References

- PwC, “Resilience through change”, 27th Annual Law Firms’ Survey, 2018, London.

- UK Jurisdiction Taskforce, “Legal statement on cryptoassets and smart contracts”, November 2019.

- The Law Society for England and Wales, “Blockchain: Legal & Regulatory Guidance”, London, September 2020.

- UK Jurisdiction Taskforce, “Digital dispute resolution rules”, London, April 2021.

- Law Commission, “Smart legal contracts, Advice to Government, London, November 2021.